Elevate Your Expertise in Data Science

Get in Touch

How to Apply

Industry Leading Faculty

Data in Action - Capstone Projects

Start Your Application

Related News, Insights, and Past Events

May

16

Upcoming EventMay 16, 2024

DSI Research Day

May

2

Upcoming EventMay 02, 2024

Data Science Clinic Student Symposium

BlogApr 25, 2024

Towards New Physics at Future Colliders: Machine Learning Optimized Detector and Accelerator Design

May

22

Upcoming EventMay 22, 2024

Chicago Data Night – Dexter Horthy (Metalytics)

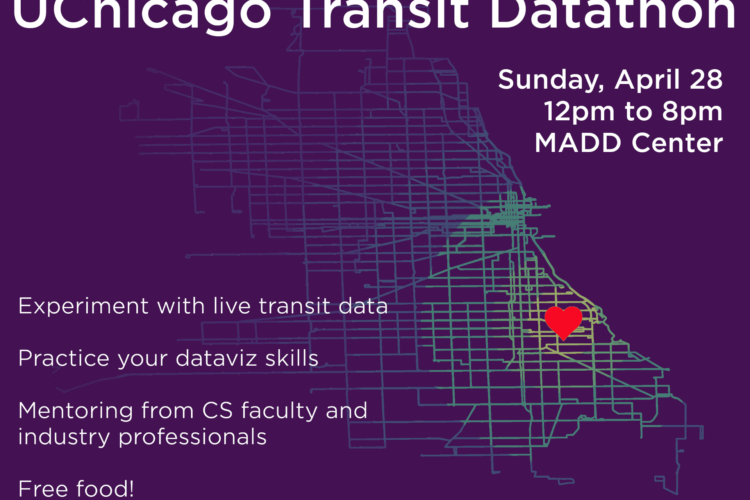

Apr

28

Upcoming EventApr 28, 2024

First Annual UChicago Transit Datathon

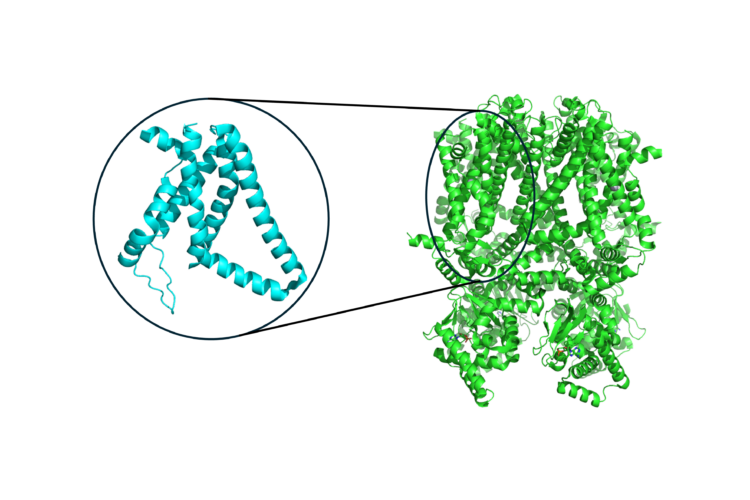

BlogApr 18, 2024

Uncovering Patterns in Structure for Voltage Sensing Membrane Proteins with Machine Learning

DSI NewsApr 18, 2024

Community Data Fellow Stephania Tello Zamudio helps broaden internet access for Illinois residents

Jun

5

Upcoming EventJun 05, 2024

Risk Assessment, Safety Alignment, and Guardrails for Generative Models

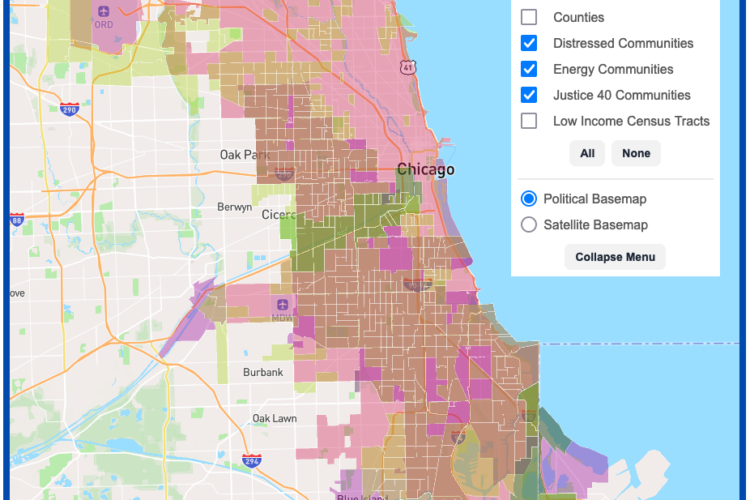

DSI NewsApr 15, 2024

DSI Software Engineers create interactive map tool to maximize climate investment tax benefits

May

21

Upcoming EventMay 21, 2024